If you are shopping to purchase a home, historically high interest rates may be scaring you off. We want to make sure that our buyers and sellers are seeing the whole picture and making the best financial decisions for their future. If you want the best results make sure you are buying a home for the right reasons and are following a comprehensive approach that considers both financial and personal factors.

Housing Affordability

One of the big factors to consider when deciding to buy a home is housing affordability. Housing affordability in March 2024 is down over 7.7% nationally compared to a year ago, according to NAR’s Housing Affordability Index, which measures whether a typical family earns enough income to qualify for a mortgage loan. Increased mortgage rates and inflation are why housing affordability is decreasing so rapidly.

Mortgage Interest Rates

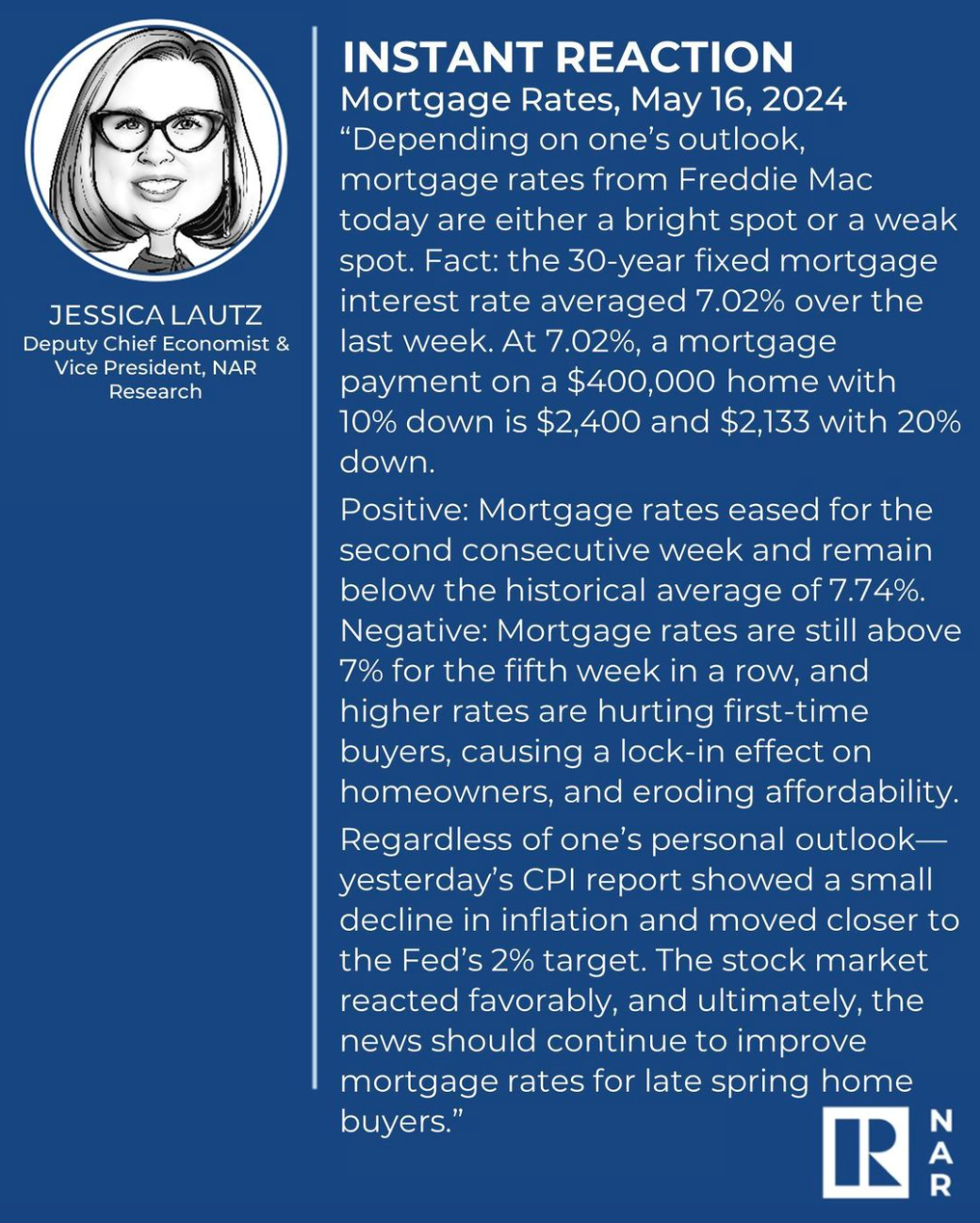

Jessica Lautz, NAR’s Deputy Chief Economist, notes that although interest rates are slightly below the historical average and inflation has slightly decreased, rates are still above 7%. This poses challenges, especially for first-time homebuyers. However, it’s important not to let rising interest rates deter you from buying a home. Waiting for rates to drop might not be realistic, especially if you have other reasons to move, such as downsizing, a job change, or a growing family.

Economic and financials are only part of the homeownership equation. Use our Comprehensive Home Buying process to consider all the factors when buying a home.

A Comprehensive Home Buying Process

1. Determine why you want to own a home.

Determine your reasons for wanting to own a home. Discuss your goals, needs, desires, and concerns with your partner to ensure alignment.

Our clients often cite these reasons: locking-in housing for the long haul, proximity to schools, having space and freedom to fulfill their plans and dreams (including the dream of owning their own home), financial asset building, and being close to family.

After meeting my wife and I, My first realtor said to us, “Oh, I see, you want TWO homes”. Before starting the home shopping journey, we hadn’t talked about what we wanted too much. When we did, it turned out we had different needs, risk tolerance levels, and ideas for the perfect home. It’s important to discuss wants, desires, and fears related to buying a home. You and your partner will probably need to compromise!

2. Get serious about your budget

Track your income and expenses to find out and fully understand where your money comes from and goes. Then, create and STICK TO your budget.

Use financial tracking software to track your income and expenses. Be sure your budget includes categories for retirement savings and, for homeowners, a plan to set aside at least 1% of the cost of your home per year for home improvements, maintenance, and repairs.

We often find there is a financial optimist and pessimist in each household. One person hawks the bills while the other wants to spend and fearlessly forge ahead. The optimist will tend to underestimate important expenses while the pessimist can be too conservative. A working budget and income/expense tracking system can get both parties on the same page.

Then, you can begin to see which homes you can comfortably afford, how much debt you are currently carrying, and how much savings you have to put towards a downpayment, closing costs, moving expenses, and new home renovations.

Beware: there are many hidden homeownership costs that first-time buyers don’t account for. Your lender will tell you how much the bank is willing to loan you; you have to decide how much debt to take on and the number can be very different.

3. Agent Up!

Hire an experienced, local real estate agent and mortgage lender. After 20 years of selling and buying homes for clients, I have seen a lot! I have some great stories, a few horror stories, and a lot of perspective on the industry and market in Ann Arbor. There are great agents and lenders in Ann Arbor who know how to help you purchase your dream home. Your job is to connect with a few and hire an agent and lender you are comfortable with.

What do you need to find out about a potential realtor?

Is this person a good listener? Do they have time for you or do they always seem unavailable? Can they negotiate well for you? Do they have resources to offer and are they connected in the community? Can they offer a systematic approach to buying a home? Do they have good ideas to share that you have not thought about? Will they answer all of your questions? Do they have testimonials and references available?

Use your agent to get at least two mortgage lender recommendations. Your agent will have a rapport with many lenders and will offer the ones that get the job done on time, are available to consult and answer questions and have a great track record.

4. Shop for your home.

Finding a great home becomes much easier once you lay the foundation using the steps above. Many home shoppers just start at step 4 and fill in the other steps as an afterthought. Finding a lender after the fact, improper research, and not understanding all the expenses will cause problems.

Helpful Resources For Planning And Budgeting

- Dave Ramsey’s 5 Steps to buying a home that won’t bust your budget guides you on how to calculate a “pre” and “post” home purchase budget. Use this to determine how much you can truly afford in a mortgage payment and taxes.

- The Michigan Property Tax Estimator: This tool helps you calculate the estimated property taxes or home at a given price. Provided by the Michigan Department of Treasury it is one of the most accurate at-home resources for calculating taxes.

- Piper Partners Blog: How Much Does It Cost To Buy A House? – Consider All The Expenses: In this comprehensive guide to buying a house, we help identify and calculate some of the hidden costs of a real estate transaction such as loan origination fees, down payments, inspection fees, and closing costs.

- Piper Partners Neighborhood Pages: We offer dedicated pages for 100’s of neighborhoods. You can view active and closed listing data and subscribe to updates.

- Piper Partners Blog: 6 Questions To Ask When Interviewing a Buyers Agent : This post gives some example questions to ask agents as you interview them; Questions that challenge their local area knowledge and expertise!

- Piper Partners Blog: The Ten Reasons People Buys And Sell Homes: In this article, we will go through the 10 reasons people make a move and our advice for each situation.